Gold prices dropped to less than $4,400 an ounce on Monday as they fell for a fourth week. The precious metal fell by 3.8% to near $4,320.30 an ounce as it erases its previous gains.

This comes as the U.S.-Iran war continues to worsen. President Donald Trump recently threatened to strike Iran's power plants if they did not reopen the Strait of Hormuz. In response, Iran threatened to attack important US and Israeli installations in the region if its energy facilities are hit.

Last time, the value of gold declined as sharply as this in a week was in 1983. In that year, oil-producing countries in the Middle East sold their gold reserves as their oil revenues declined. The same region has caused a similar crash in the market as it did over 40 years ago.

The key question now is, how did this derail gold's earlier bullish run? While we have enjoyed record highs in the asset since last year, it is now falling faster than expected. In other words, how exactly are the Middle East oil tensions actually weighing the precious metal down ?

Why Exactly Do Gold Prices Drop When Oil Tensions Rise

Normally, in times of turmoil, investors tend to invest in gold, as it is expected that it will hold its value in case of a rise in inflation, a fall in currencies, or a crisis.

However, rising energy prices due to the Middle East conflict are causing central banks across the globe to reassess their interest rate outlook. The factor is particularly important because of its impact on assets.

This is mainly because gold does not pay interest. With a rise in real yields and the dollar, gold becomes increasingly less attractive compared to Treasury bonds. The 10-year yields rose to 4.2 % this week. The Dollar Index also rose to 99.9. This has negated whatever safe-haven appeal the conflict might have created.

Also, in times of major energy crises, the stock markets tend to panic. Large investors, in times of “margin calls” (losses in their existing investments), sell their gold, which is a liquid asset easily convertible to cash in an instant, to pay off their dues.

Fed's Reaction to Oil Shocks Could Crush Gold

The 80% jump in oil prices since the conflict began has definitely created a new inflation shock for global economies, which had been finding it difficult to get inflation under control.

This has left central banks and the Fed in a tricky position. This is higher oil prices translate directly into higher consumer prices, which means inflation will be more persistent, keeping interest rates higher for longer.

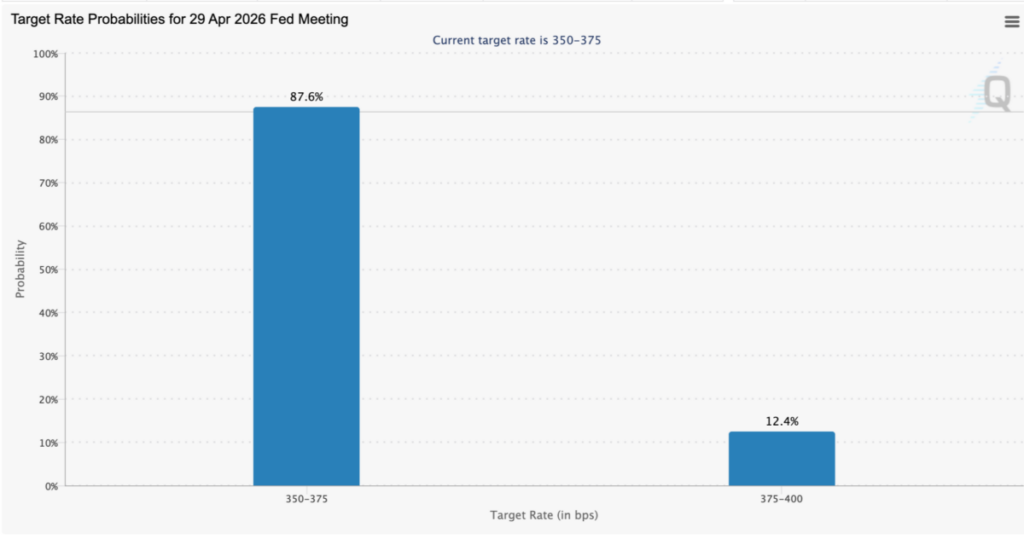

Traders now think the Federal Reserve will keep interest rates steady this year, which will boost bonds as an attractive investment but hurt gold, which does not pay investors anything.

Usually, Fed interest rates have a major impact on the markets. The Fed has kept its interest rates steady for the second meeting running. Traders are now betting that there will be no further interest rate cuts this year, according to the CME FedWatch tool.

Gold prices went through the roof during the last fall as the Fed cut its interest rates three times consecutively. Now, Fed interest rates are expected to remain steady for a few more months, which has caused bond yields to rise, making gold less attractive as an investment.

What All This Means for Your Gold Strategy

Gold rose by 64% in 2025, its best performance since 1979. The precious metal touched $5,000 an ounce for the first time in January.

Quite frankly, this hype is rapidly dying down. The rally in gold in recent months has been partly driven by retail investors jumping on the bandwagon. But the asset has been behaving more like a meme coin than a safe haven as at press time.

Also, Gold ETFs have lost over 60 tonnes in the last three weeks. The institutional selling is real, not just profit-taking. In fact, some analysts have termed the current gold price movement as “suspended in open air.”

On the other hand, some analysts have pointed out that the funds invested in gold’s rally to $1,500 in 2025 were not invested in a long-term bet. They were invested in the momentum trade, which is now leaving. Historically, this has been a catalyst for upward price moves in the asset.

When the metal prices fall sharply, retail investors sell, hedge funds cover their margins, and the media announces the end of the rally. Central banks, however, continue to buy.

For instance, when gold declined by 20% from its peak in 2022, central banks responded by buying 1,082 tonnes. In 2023, when interest rates rose and ETF investors reduced their holdings, Central banks stepped in to fill the gap. In 2024, they added another 1,045 tonnes.

Interestingly, the major bank forecasts are still bullish. J.P. Morgan (JPM) predicted a year-end price of $6,300 for 2026, driven by central bank demand and ETF inflows. Wells Fargo also forecasted a range of $6,100 to $6,300. Essentially, this suggests its rebound might be as strong as its decline.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment