Sector rotation sounds simple: own the strongest areas of the market and avoid the weakest. The results, however, are anything but uniform.

A review of six managed and model-based sector-rotation strategies, as shown in the table below, found outcomes ranging from modest returns with limited drawdowns to triple-digit gains with much larger drawdowns.

| Model # | Portfolio Name | Ticker or ID | 1-year total return | 1-year max drawdown | 10-year total return (annualized) | 10-year max drawdown |

| 1 | Sector Rotation Fund | NAVFX | 16.3% | 6.3% | 11.6% | 22.3% |

| 2 | The First Trust Dorsey Wright Focus 5 | FV | 26.5% | 9.0% | 13.2% | 20.1% |

| 3 | Top 3 Sector Rotation | t.srt3 | 36.0% | 4.4% | 12.6% | 20.2% |

| 4 | Top 5 Sector Rotation | t.srt5 | 54.4% | 3.2% | 18.2% | 16.3% |

| 5 | Relative Strength Sector Rotation | t.srrs | 18.3% | 4.3% | 11.2% | 11.9% |

| 6 | Quartile Sector Rotation | t.srqr | 114.0% | 13.9% | 29.3% | 50.7% |

| – | Benchmark: SPDR S&P 500 ETF | SPY | 29.8% | 5.8% | 15.6% | 23.9% |

Managed Funds Did Not Deliver A Clear Edge

Sector Rotation Model 1 is the aptly named mutual fund “Sector Rotation Fund” (NAVFX), managed by Grimaldi Portfolio Solutions. The fund charges 2.04% annually, including acquired-fund expenses, according to its prospectus. Its strategy uses sector, broad-market, international and inverse ETFs, and the fund reported portfolio turnover of 136.35% for its latest fiscal year.

In the risk-and-return review, NAVFX did not show a clear advantage over the S&P 500, based on a comparison to the SPDR S&P 500 ETF (NYSE:SPY). NAVFX’s average return was 4 percentage points below SPY, and NAVFX’s max drawdown was only 1.6% less than SPY over the past 10 years. That’s not enough of a risk reduction to justify the lower return.

Sector Rotation Model 2 is the First Trust Dorsey Wright Focus 5 ETF (NASDAQ:FV). As an exchange-traded fund, it’s less expensive, with a 0.89% total expense ratio. It’s a fund-of-funds, holding five First Trust sector or industry ETFs. But convenience has not translated into benchmark-beating performance. First Trust reported a 10-year annualized NAV return of 13.2% through May 2026, compared with 15.6% for the S&P 500 Index.

More Holdings Improved The Momentum Model

Sector Rotation Model 3 is the Top 3 Sector Rotation (ID: t.srt3). This model portfolio’s algorithm ranks a set of Fidelity Select sector funds by momentum over the past year. Then the model picks the top three funds to buy. Over the past 10 years, this “Top 3 Sector” model has returned 12.6% (annualized) with a maximum drawdown of 20.2%.

Sector Rotation Model 4 is similar to Model #3, but holds the top five ranked sector funds. This more diversified approach produced a stronger historical result. Over the past 10 years, the Top 5 model returned 18.2% annualized with a 16.3% maximum drawdown. So adding two holdings improved return and reduced drawdown. This model portfolio also beats NAVFX, FV, and t.srt3 in terms of both total return and risk (as measured by maximum drawdown).

Defense Versus Concentration

Sector Rotation Model 5 is a Relative Strength Sector Rotation Portfolio (ID: t.srrs) which uses a set of sector ETFs as its investment universe. This approach applies a 10-month return measure and a 10-month moving average. Funds that fall below the moving average are excluded, and the portfolio can move partly or entirely to cash if no sectors are above their 10-month moving averages.

Its 10-year historical result was an 11.2% annualized return with a 11.9% maximum drawdown. It has lagged the S&P 500 over the last five years, but its defensive rule materially reduced the worst historical decline. Its maximum drawdown is the lowest in this list.

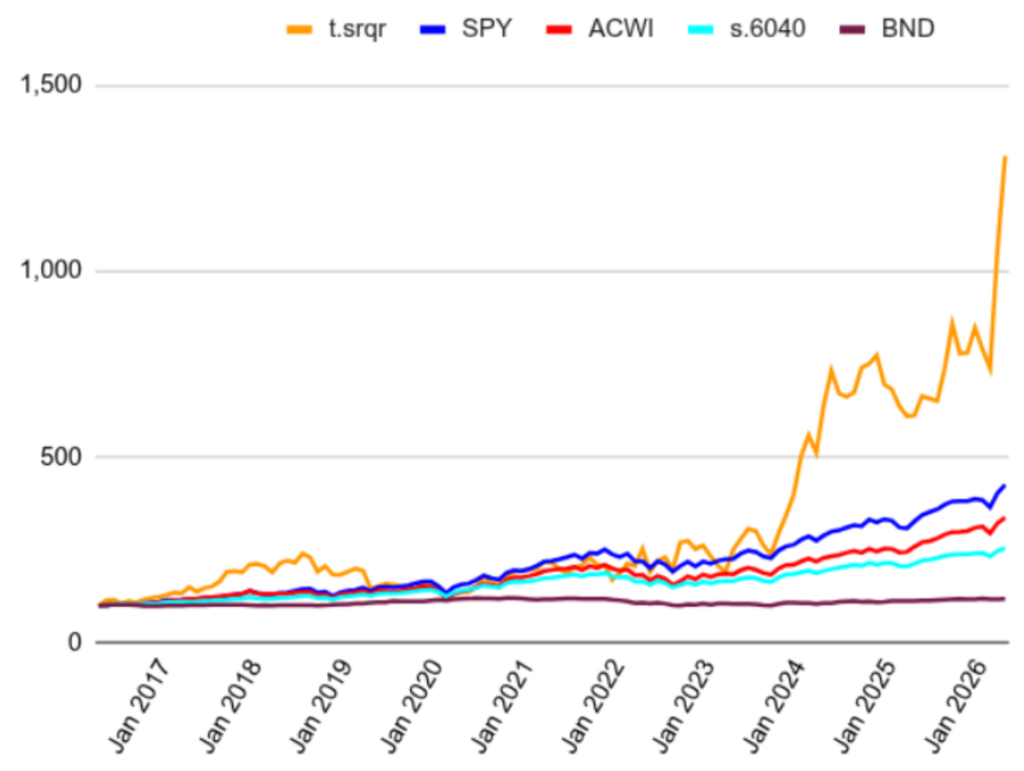

Sector Rotation Model 6 is the Quartile Sector Rotation Portfolio (ID: t.srqr). This model lies at the other extreme of risk and return. This model selects from over 100 sector funds and owns only one at a time. This concentrated approach has produced a quite notable 114% one-year gain and a 29.3% annualized 10-year return. Over the past decade, t.srqr has far outpaced major benchmarks, as the chart below shows. However, in the past 10 years it’s also seen a 50.7% maximum drawdown (based on month-end total return).

10-Year Normalized Total Return: t.srqr vs. Benchmarks

This t.srqr model has more than doubled in the past year. But over the past decade, it’s also exposed investors to drawdowns large enough to test their ability to remain invested.

What Investors Should Ask

“Sector rotation” describes a broad idea, not a uniform investment product. These six models we’ve looked at show this. Before comparing sector rotation strategies, funds, and model portfolios, investors should ask:

- How many holdings can the portfolio own?

- What momentum lookback period does it use?

- How often does it rebalance?

- Can it move to cash?

- What are the fund fees, trading costs and tax consequences?

- Are the reported results live, backtested or a combination of both?

The label matters less than the rules. In this review, FV offered the cleaner hands-off option, the Top 5 model (t.srt5) provided the strongest balance among the diversified models, the relative-strength model (t.srrs) offered the best drawdown control, and the quartile model (t.srqr) delivered the highest return with the greatest concentration risk.

Disclosure And Methodology

Disclosure: The author has no financial ties with ETFs and mutual funds covered. The author’s firm, RecipeInvesting.com, publishes four of the six model portfolios discussed (t.srqr, t.srrs, t.srt5, t.srt3).

Methodology: Results reflect month-end total-return data through May 31, 2026. The RecipeInvesting model portfolios (t.srqr, t.srrs, t.srt5, t.srt3) have been published monthly since June 2016, so their 10-year results are live, out-of-sample history. Model returns reflect the expenses of the underlying funds held but do not include trading costs, slippage, or taxes. The returns assume monthly rebalancing. NAVFX and FV are independently managed funds; their results are actual returns net of fund expenses, as reported by the fund sponsors. Past performance does not guarantee future results.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment