President Donald Trump accused Iran of violating the ceasefire on Friday after saying Tehran launched at least four one-way attack drones at ships transiting the Strait of Hormuz, including one that struck the upper deck of a cargo vessel.

“Obviously, this is a foolish violation of our Ceasefire Agreement,” Trump wrote on Truth Social, adding that U.S. forces shot down three of the drones while the damaged ship was able to continue its voyage.

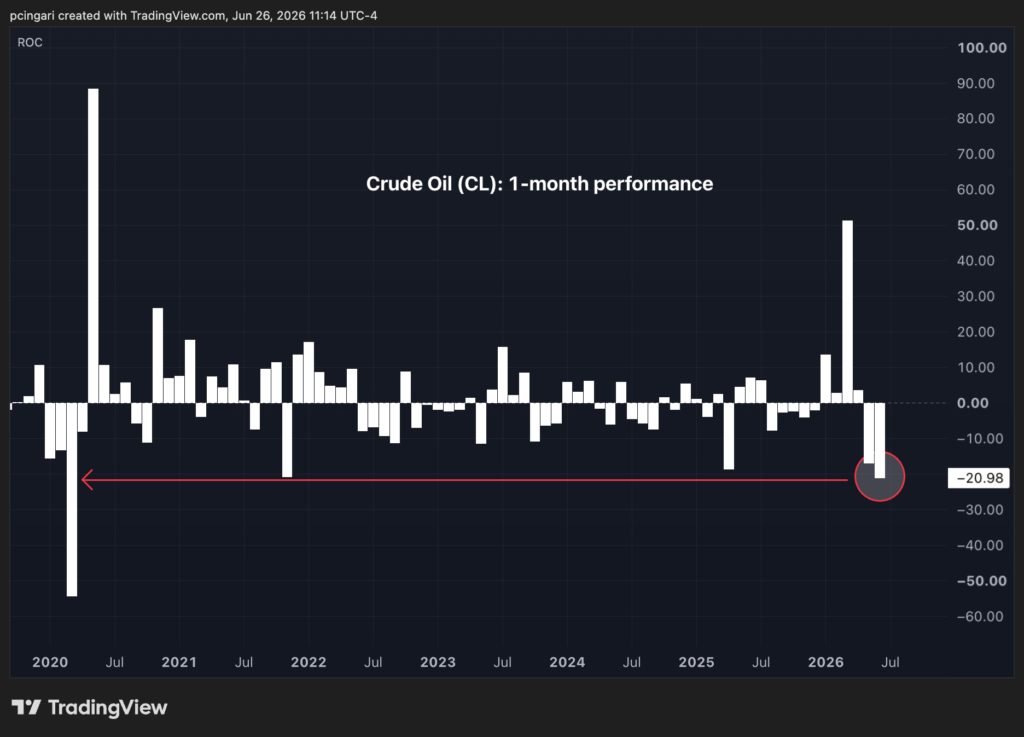

Weeks ago, that would have launched crude. This time, the market barely flinched.

The war premium that was supposed to keep crude bid for years has now fully evaporated.

Despite Trump’s warning, oil is now on pace for its worst month since March 2020, with Gulf supply returning faster than anyone modeled.

West Texas Intermediate — as tracked by the United States Oil Fund (NYSE:USO) — dropped to around $69 a barrel Friday, extending a selloff that has unwound most of the Strait of Hormuz spike.

Crude’s month-to-date performance is now down by 21% — the deepest monthly drop since the COVID-19 pandemic crash of March 2020.

The market has stopped pricing scarcity. It has started pricing a glut.

Chart: Crude’s Worst Month In Over Six Years

Gulf Supply Is Returning Faster Than Expected

Gulf barrels are coming back, and quickly.

Total Persian Gulf exports have climbed back to 63% of normal levels on a seven-day basis, according to Goldman Sachs commodities research led by Yulia Zhestkova Grigsby.

There have been no reported attacks on shipping near the Strait of Hormuz since June 11.

The U.S. Treasury has issued a 60-day waiver authorizing Iranian oil sales, a move Goldman estimates could unlock as much as 60 million barrels of Iranian crude already sitting on water.

With the supply returning, the market is fast-forwarding.

According to Goldman Sachs, the market is “already pricing expected future surpluses.”

The clearest tell sits in the curve. Dubai prompt timespreads have flipped into contango, which is when near-term barrels now trade cheaper than later-dated ones — the textbook signature of a market that expects oversupply rather than scarcity.

China Is Weakening The Demand Story

At the same time, the world’s largest importer is consuming less crude.

In a note shared Friday, Ed Yardeni indicated that one reason oil never fully reflected the geopolitical risks around the Strait of Hormuz is China’s structural demand slowdown.

After roughly three decades of almost uninterrupted growth, Chinese crude imports fell to just 4.6 million barrels per day in May, weighed down by rapid EV adoption, a prolonged property downturn, slower economic growth and elevated inventories.

According to JPMorgan, China accounts for roughly 74% of the recent decline in global crude imports.

The Geopolitical Premium Is Disappearing

Goldman indicated investors are beginning to question whether crude deserves the geopolitical premium it has carried since the conflict began.

The speed with which exports have recovered — and the market’s ability to reroute supply while demand adjusts — has challenged the assumption that long-dated oil prices must permanently embed elevated security risks.

In other words, traders are no longer paying for what could happen. They’re reacting to what is happening.

Lower oil prices could also provide a tailwind for the broader economy.

Oxford Economics expects falling crude prices to reduce bunker fuel costs, ease freight rates and gradually relieve supply-chain pressures, while also helping to moderate fertilizer prices and broader inflationary pressures over the coming months.

Login to comment